Published February 18, 2025

Your Credit Report: Interpret, Access and Use it!

Your credit report tells potential lenders how responsible you’ve been with credit in the past. When you apply for credit, lenders can legally request this document from one or more of the credit bureaus (Experian, Equifax and TransUnion) to assess how risky it is to lend to you.

What can lenders see on your credit report?

Your credit report provides a detailed summary of your credit history. It includes your personal information and lists details on your past and current credit accounts. It also documents each time you or a lender requests your credit report, as well as instances where your accounts have been passed on to a collection agency. Financial issues that are part of the public record, such as bankruptcies and foreclosures, are included, too.

How to access your report

You can request a free copy of your credit report from each of three major credit reporting agencies – Equifax®, Experian®, and TransUnion® – once each year at AnnualCreditReport.com or call toll-free 1-877-322-8228. You’re also entitled to see your credit report within 60 days of being denied credit, or if you are on welfare, unemployed, or your report is inaccurate.

It’s a good idea to request a credit report from each of the three credit reporting agencies and to review them carefully, as each one may contain inconsistent information or inaccuracies. If you spot an error, request a dispute form from the agency within 30 days of receiving your report. If there are errors on your credit report, you should take the steps necessary to fix them. Although your credit score is helpful, it doesn’t tell the full story. Identify any gaps in your credit report and be prepared to explain the cause of those gaps to your lender….this goes a long way.

What does a credit score mean?

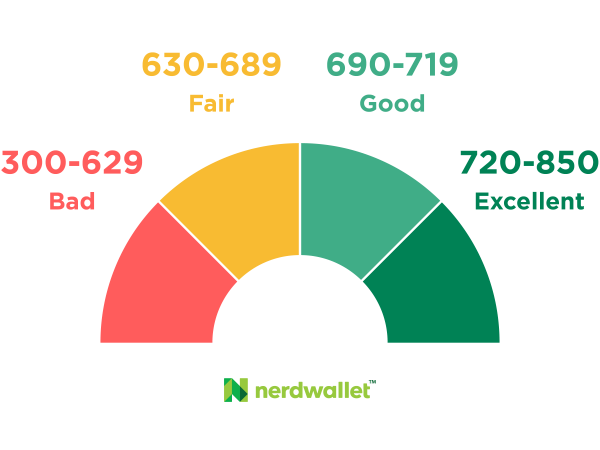

Your credit score is a numerical representation of your credit report that represents your creditworthiness. Scores can also be referred to as credit ratings, and sometimes as a FICO® Credit Score, created by Fair Isaac Corporation, and typically range from 300 to 850.

FICO® Scores are comprised of five components that have associated weights:

Payment history: 35%

Amounts owed: 30%

Length of credit history: 15%

How many types of credit in use: 10%

Account inquiries: 10%

Lenders use your credit score to evaluate your credit risk – generally, the higher your credit score, the lower your risk may be to the lender.

Responsibility is key

Above all, it’s important to use credit responsibly. A good credit history and credit score can be the difference between being able to purchase a home, buy a car, or pay for college. Proactively managing your credit report is a great way to stay in control of your finances, and ultimately achieve your goals.

How your credit score is calculated

Learn what your credit score is based on and the many ways you can improve it.

Your credit score is one of the most important measures of your creditworthiness. For your FICO® Credit Score, it's a three digit number usually ranging between 300 to 850 and is based on metrics developed by Fair Isaac Corporation. The higher your score is, the less risky you are to lenders. By understanding what impacts your credit score, you can take steps to improve it.

The five pieces of your credit score

Your credit score is based on the following five factors:1

Your payment history accounts for 35% of your score. This shows whether you make payments on time, how often you miss payments, how many days past the due date you pay your bills, and how recently payments have been missed. Payments made over 30 days late will typically be reported by your lender and hurt your credit scores. How far behind you are on a bill payment, the number of accounts that show late payments and whether you've brought the accounts current are all factors. The higher your proportion of on-time payments, the higher your score will be. Every time you miss a payment, you negatively impact your score.

How much you owe on loans and credit cards makes up 30% of your score. This is based on the entire amount you owe, the number and types of accounts you have, and the proportion of money owed compared to how much credit you have available. High balances and maxed-out credit cards will lower your credit score, but smaller balances can raise it – if you pay on time. New loans with little payment history may drop your score temporarily, but loans that are closer to being paid off can increase it because they show a successful payment history.

The length of your credit history accounts for 15% of your score. The longer your history of making timely payments, the higher your score will be. Credit scoring models generally look at the average age of your credit when factoring in credit history. This is why you should consider keeping your accounts open and active. It may seem wise to avoid applying for credit and carrying debt, but it can actually hurt your score if lenders have no credit history to review.

The types of accounts you have make up 10% of your score. Having a mix of accounts, including installment loans, home loans, and retail and credit cards may help improve your score.

Recent credit activity makes up the final 10%. If you’ve opened a lot of accounts recently or applied to open accounts, it may suggest potential financial trouble and may lower your score. However, credit scoring models are also built to recognize that consumers who are shopping for a loan aren't necessarily extra risky.

Ultimately, the best way to help improve your credit score is to use loans and credit cards responsibly and make prompt payments. The more your credit history shows that you can responsibly handle credit, the more willing lenders will be to offer you credit at a competitive rate.